FIFO, preferred under IFRS, showcases a stronger financial position by reporting lower COGS and thus higher net income, beneficial during inflation. Enhancing investor and lender perceptions by reflecting current casualty and theft losses definition market prices in inventory valuation may be most desirable in industries where asset valuation impacts financial health. Under FIFO, inventory stock tends to be closely aligned with current market costs.

Company

This can happen when product costs rise and those later numbers are used in the cost of goods calculation, instead of the actual costs. The “inventory sold” refers to the cost of purchased goods (with the intention of reselling), or the cost of produced goods (which includes labor, material & manufacturing overhead costs). Implementing FIFO can also be complex, requiring meticulous inventory tracking and management procedures that can be resource-intensive. Warehouse managers must ensure accurate inventory labeling and tracking, implement effective inventory storage solutions, and ensure staff rotates inventory based on receiving dates.

FIFO Inventory Method Explained

Sometimes, companies will opt to use FIFO internally because it shows the physical flow of goods. But, they will use LIFO for financial reporting purposes because it typically offers a lower income tax expense. The FIFO or LIFO reserve is the difference between LIFO inventory and FIFO inventory.

Simplified Cost Calculation

This results in deflated net income costs and lower ending balances in inventory in inflationary economies compared to FIFO. Assume a company purchased 100 items for $10 each and then purchased 100 more items for $15 each. The COGS for each of the 60 items is $10/unit under the FIFO method because the first goods purchased are the first goods sold. Of the 140 remaining items in inventory, the value of 40 items is $10/unit and the value of 100 items is $15/unit because the inventory is assigned the most recent cost under the FIFO method.

What Is The FIFO Method? FIFO Inventory Guide

Aided by inventory software, the simplicity of FIFO helps reduce errors and enhance operational efficiency. FIFO encourages the rotation of stock, which can lead to better inventory quality overall. Customers receive products that are fresher or more current, which can enhance customer satisfaction and reduce the need for markdowns and waste. In this deep dive into FIFO inventory management, we will answer all of these questions and more, highlighting important use cases and the strategic value it offers.

- This discrepancy can result in misleading financial statements that don’t accurately reflect the company’s true financial position or operational challenges.

- In LIFO, however, balance sheet results may underrepresent the current value of inventory if prices have risen.

- Whereas FIFO assumes that the oldest items added to inventory are the first sold, LIFO assumes that the most recently acquired inventory is sold first.

- The FIFO method of inventory management aligns new orders with oldest inventory to ship first to decrease distribution of outdated or expired goods.

- But for accounting purposes, the grocery store assumes that the first oranges sold were from the beginning inventory.

FIFO usually aligns more closely with the actual movement of goods in most businesses. In these sectors, rapid price fluctuations can lead to a significant mismatch between reported profits and actual inventory replacement costs. FIFO method assumes that the earliest acquired items are the first to leave inventory, regardless of their actual usage order. The FIFO inventory valuation method is widely applied across industries, particularly when managing goods with short shelf lives or rapidly evolving technologies. FIFO (First-In, First-Out) aligns with this principle by serving as a critical framework in inventory management and accounting.

To calculate COGS (Cost of Goods Sold) using the FIFO method, determine the cost of your oldest inventory. Let’s say a grocery store buys oranges at the beginning of the week and at the end of the week. Extensiv also enables real-time visibility into inventory levels and product aging, facilitating FIFO adoption. Whether you’re using FIFO, LIFO, accurate cost, or some other inventory management method, Extensiv can help you streamline and optimize inventory management, warehousing, and shipping processes. He has a CPA license in the Philippines and a BS in Accountancy graduate at Silliman University. Many businesses use FIFO, but it’s especially important for companies that sell perishable goods or goods that are subject to declining value.

In times of rising prices, LIFO results in higher COGS due to the use of newer, more expensive inventory, which can lower taxable income and thus, tax liabilities. While LIFO also impacts a company’s financial health and tax obligations, LIFO differs significantly in regard to accounting practices and financial reporting. Help with inventory management is one of the many benefits to working with a 3PL. You can read DCL’s list of services to learn more, or check out the many companies we work with to ensure great logistics support. When the price of goods increases, those newer and more expensive goods are used first according to the LIFO method. This increases the overall cost of goods sold and leaves the cheaper, earlier purchased goods as inventory, which may end up not even being sold under the LIFO model.

This can help ensure timely inventory delivery and accurate product documentation. You should also create clear communication channels with your suppliers about FIFO requirements and expectations. Fulfillment software with supplier management capabilities can help you and stakeholders track supplier performance, monitor delivery schedules, and communicate effectively. Additionally, demand forecasting and inventory planning tools can help you plan for future inventory needs and coordinate replenishment to maintain optimal inventory levels. It can be easy to lose track of inventory, so adopt a practice of recording each order the day it arrives. This makes it easier to accurately account for your inventory and maintain proper FIFO calculations.

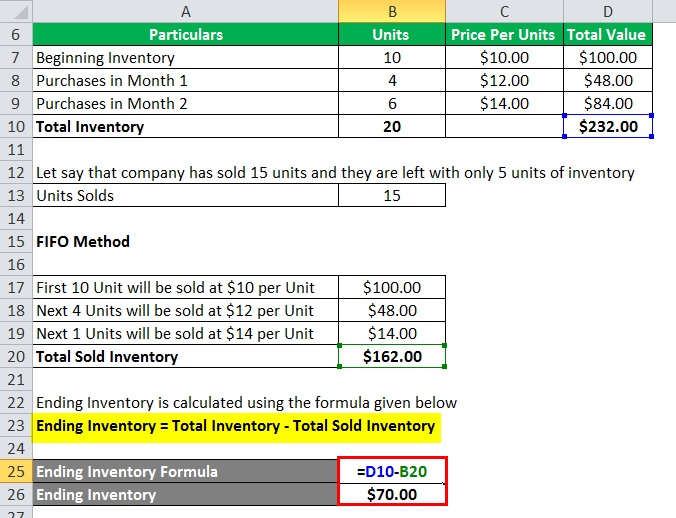

We serve the needs of affordable housing, construction, family-owned businesses, healthcare, manufacturing and distribution, and nonprofit industries. We also assist service organizations with the full suite of SOC services (including SOC 2 reports), HiTrust CSF, internal audits, SOX compliance, and employee benefit plan audits. Thus, the above example of FIFO inventory method gives a clear idea about the valuation process. But FIFO has to do with how the cost of that merchandise is calculated, with the older costs being applied before the newer. This is often different due to inflation, which causes more recent inventory typically to cost more than older inventory. Jami Gong is a Chartered Professional Account and Financial System Consultant.