This method often leads to more current inventory valuation and can affect key financial ratios used by investors and analysts. Implementing the First-In, First-Out (FIFO) method effectively can significantly improve your inventory management and financial reporting. Here are key best practices to ensure successful implementation of the FIFO inventory valuation method. FIFO, or First In, First Out, is an inventory valuation method that assumes that inventory bought first is disposed of first.

FIFO: Periodic Vs. Perpetual

In LIFO, however, balance sheet results may underrepresent the current value of inventory if prices have risen. In environments where inflation or rising costs are a factor, FIFO can show higher profits by selling older, less expensive inventory first. FIFO’s ability to impact the bottom line in the short term offers a more attractive financial position to investors and stakeholders. The controller uses the information in the above table and the FIFO inventory method formula to calculate the cost of goods sold for December and the inventory balance as of the end of December. The Periodic FIFO method can be simpler to implement than the perpetual system, as it doesn’t require constant tracking of inventory. However, it may not provide the most accurate picture of inventory levels and COGS during the accounting period, as it only updates these figures at the end of the period.

Use The Right Accounting Software

- You can use fulfillment software to assign and track FIFO-related tasks, while workflow automation can streamline training processes and ensure consistency for FIFO implementation.

- Some companies choose the LIFO method because the lower net income typically leads to lower income taxes.

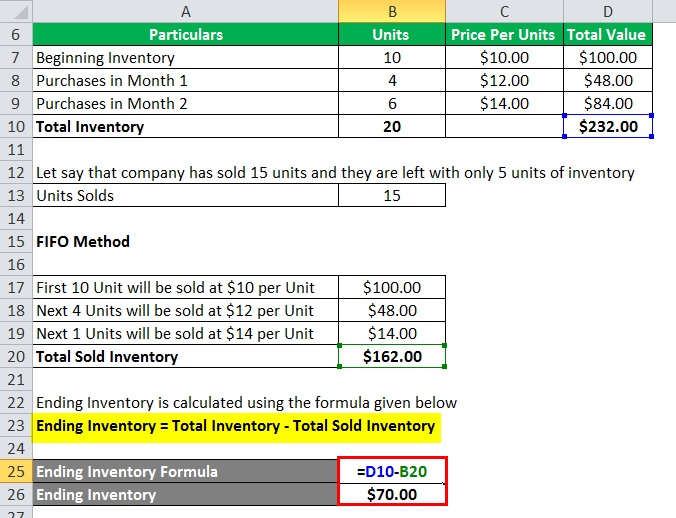

- First-in, first-out (FIFO) is one of the methods we can use to place a value on the ending inventory and the cost of inventory sold.

As the price of labor and raw materials changes, the production costs for a product can fluctuate. That’s why it’s important to have an inventory valuation method that accounts for when a product was produced and sold. FIFO accounts for this by assuming that the products produced first are the first to be sold or disposed of.

Medical Device Manufacturing: Ensuring Compliance and Safety

It’s recommended that you use one of these accounting software options to manage your inventory and make sure you’re correctly accounting for the cost of your inventory when it is sold. This will provide a more accurate analysis of how much money you’re really making with each product sold out of your inventory. Inventory is typically considered an asset, so your business will be responsible for calculating the cost of goods sold at the end of every month. With FIFO, when you calculate the ending inventory value, you’re accounting for the natural flow of inventory throughout your supply chain. This is especially important when inflation is increasing because the most recent inventory would likely cost more than the older inventory. This method dictates that the last item purchased or acquired is the first item out.

Seamless integration between inventory management and accounting systems ensures FIFO calculations are correctly reflected in financial reports. This provides real-time cost of goods sold figures, improves the accuracy of profit calculations, and simplifies the financial reporting process. In times of rising prices, FIFO results in higher reported earnings because it pairs current sale prices with inventory purchased at earlier, lower costs.

First, we add the number of inventory units purchased in the left column along with its unit cost. In this lesson, I explain the FIFO method, how you can use it to calculate the cost of ending inventory, and the difference between periodic and perpetual FIFO systems. The costs of buying lamps for his inventory went up dramatically during the fall, as demonstrated under ‘price paid’ per lamp in November and December.

It can also refer to the method of inventory flow within your warehouse or retail store, and each is used hand in hand to manage your inventory. Alternative methods include LIFO, Weighted Average Cost, Specific Identification, and Standard Costing. LIFO assumes the newest inventory is sold first, resulting in a higher cost of goods sold during inflation. Specific Identification tracks individual item costs, while Standard Costing uses predetermined values while adjusting for variances over time. FIFO impacts financial statements by typically reporting higher profits during inflation. It results in lower cost of goods sold and higher ending inventory values on the balance sheet.

Sal’s Sunglasses is a sunglass retailer preparing to calculate the cost of goods sold for the previous year. Average cost inventory is another method that assigns the same cost to each item and results in net income and ending inventory balances between FIFO and LIFO. Inventory is assigned costs as items are prepared for sale and based on the order in which the product was used. On the basis of FIFO, we have assumed that the guitar purchased in January was sold first.

You can use fulfillment software to assign and track FIFO-related tasks, while workflow automation can streamline training processes and ensure consistency for FIFO implementation. Accounting standards are only concerned with cost flow assumptions as they affect inventory valuation in the financial statements. Good inventory management software makes it easy to log new orders, record prices, and calculate FIFO.

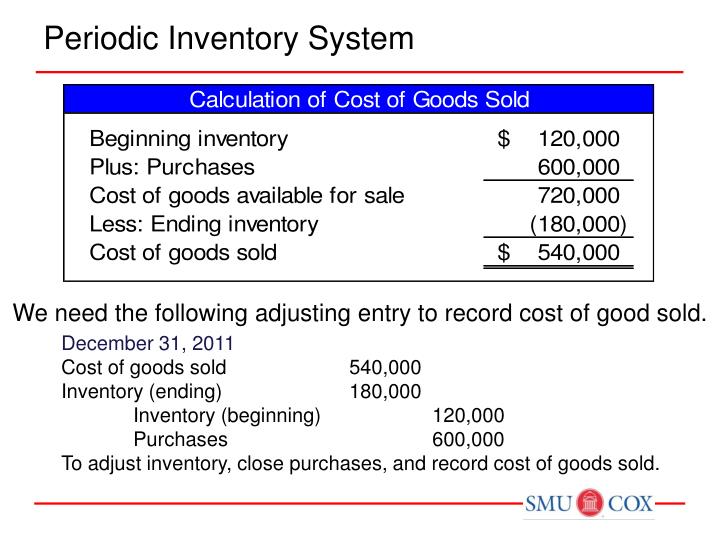

Not only is net income often higher under FIFO but inventory is often larger as well. Accurate record-keeping ensures that you have a clear, real-time understanding of your inventory levels, costs, and movements. Without precise records, it’s deducting education expenses in 2020 impossible to correctly apply FIFO principles, which can lead to errors in financial reporting and inventory valuation. The company makes a physical count at the end of each accounting period to find the number of units in ending inventory.

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Additionally, LIFO’s reception varies globally, with some accounting standards discouraging its use, thereby limiting its applicability for international businesses.